Critical Materials and Why They Matter

Making Sense of Troubling Times: By Monique Kelly

This piece may feel a little overwhelming, but to find solutions we first need to understand the problem. It will run through the challenges we’re facing, but most importantly some of the solutions we can start to put into practice. There are lots of links for those who want to find out more. Some of it is technical so please jump that section if you feel the need. Make sure that if you do feel overwhelmed, reach out to a friend for a good chat, go for a walk in nature, get out and do some physical work, watch a cheesy 90s romcom, go for a run or do a sudoku. Whatever you need to do to settle your mind. It is a long read so before you start, put the kettle on and make yourself a cuppa, take a big breath, exhale and know that we will be ok. Humans have an incredible capacity to adapt to change.

THE CHALLENGE

In the previous article, we’ve looked at the impact of the conflict in the Gulf on food systems and energy systems. This time, we’re going to look at the flow of critical materials and what this means for the built environment, manufacturing and supply of goods.

We live in a material world. Over the past 100 years, a small blip in the lifespan of our species, we have created an increasingly complex and extractive system that is consuming materials at an accelerating pace. This is a finite reality, and we need to start thinking differently if we are to provide future generations with options. But to find the right solutions, we first need to understand the problem.

How The Age of Oil Has Supercharged a Material World

In the past, civilisations have been defined by the materials that shaped them. Think the Stone Age, Iron Age, etc. Our civilisation could possibly be defined by more than just one, the Age of Plastics included. Most likely, we will be known as The Age of Oil.

All physical resources on Earth are finite. This includes oil, metals, minerals, and biological resources. While some resources can be replaced over time, many take millions of years to form so effectively outside any human timeframe. For example, the oil extracted today is the result of organic matter buried deep within the Earth, transformed over millions of years by immense pressure and heat. The copper we use in buildings and electrical wires forms over millions of years as molten rock and mineral-rich fluids cool and concentrate metals deep within the Earth’s crust.

Oil is arguably the most critical material in the current system and remains the largest commodity market in the world. It is embedded across almost every stage of the industrial system, acting both as a material in its own right, such as in plastics and fertilisers, and as an enabler for producing and moving other materials. It fuels the machinery used to extract resources, the ships and trucks that transport them, and many of the industrial processes used to refine and manufacture goods. Even where renewable energy is used, the infrastructure required to generate, build, and maintain that energy system still depends heavily on materials and supply chains that are currently linked to fossil fuels. If you want to find out more about oil as a critical material, check out our other articles on Fuel, Food, Climate and the Fragility of Our System and Understanding the Energy System We Built Our World On, and What Comes Next.

In this article, we’re going to have a look at some of the other critical materials that shape our world and are essential to the maintenance of the energy intensive, complex system we have created over the last 200 years. For a deeper exploration into materials, check out Material World by Ed Conway or Balazs Matics’ The Honest Sorcerer substack.

Understanding How Materials Flow

We have built a highly complex global system to produce and deliver things. As stated above, this has been driven in large part by an easy to access, cheap, single-use ancient solar battery we’ve been able to tap into. The abundant energy has enabled us to extract raw resources from the environment, transport these, often long distances, to be refined or processed. From there, materials are shipped again to be manufactured into components, assembled into products in another location, packaged, branded, and finally sold to consumers. Materials move through particularly complex chains, involving many stages, countries, and businesses before reaching end use.

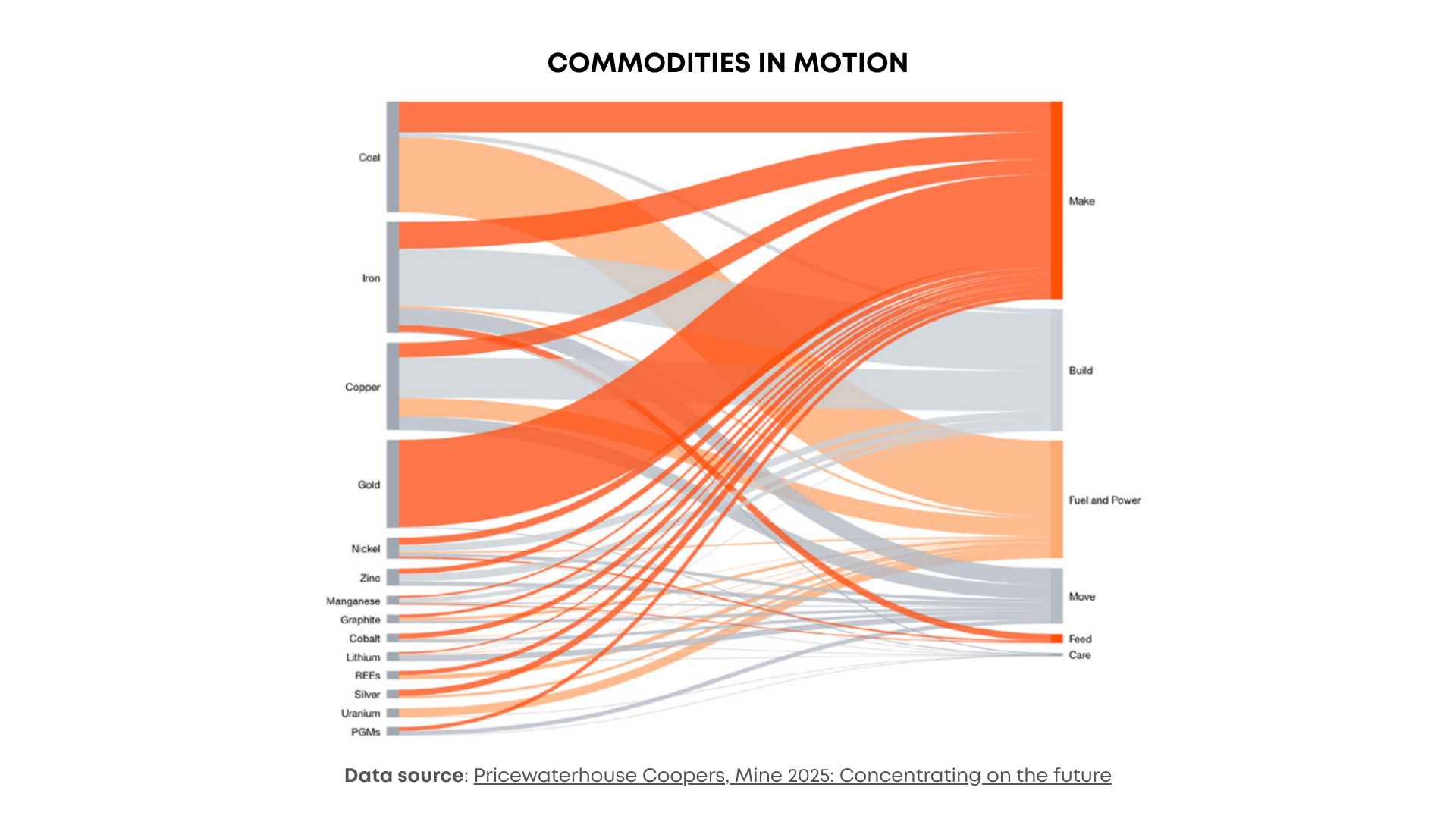

Our industrial system relies on a steady, regular flow of materials to make, build, fuel and power our communities and economy, grow and transport food, move people and goods, heat and cool our homes, provide clean water and sanitation, enable communication and digital connectivity, support healthcare and medicines, manufacture everyday goods, and maintain and expand the infrastructure we depend on.

Coal, copper and uranium underpin a large share of global electricity, with certain key minerals being essential for renewables and grid infrastructure. The shift to electric transport is driving demand for lithium, cobalt, nickel, and other battery materials. Agriculture depends on fertilisers like phosphate and potash, which rely on sulphur and sulphuric acid for production, to sustain food production. These same chemicals are also critical for processing many metals. Healthcare relies on metals such as titanium, cobalt and helium for equipment and implants. Construction uses steel, copper, aluminium, and cement inputs. Almost all manufactured goods, from your dishwasher, phone or computer to aircraft, depend on mined resources.

Efficiency, Complexity, and Fragility

The current system has been designed for efficiency and cost reduction. It relies on long, interconnected supply chains that are highly vulnerable to disruption. It also depends heavily on energy, transport, finance, and logistics systems working seamlessly together. However this system is fragile, resource intensive, and prone to cascading impacts when any part is disrupted.

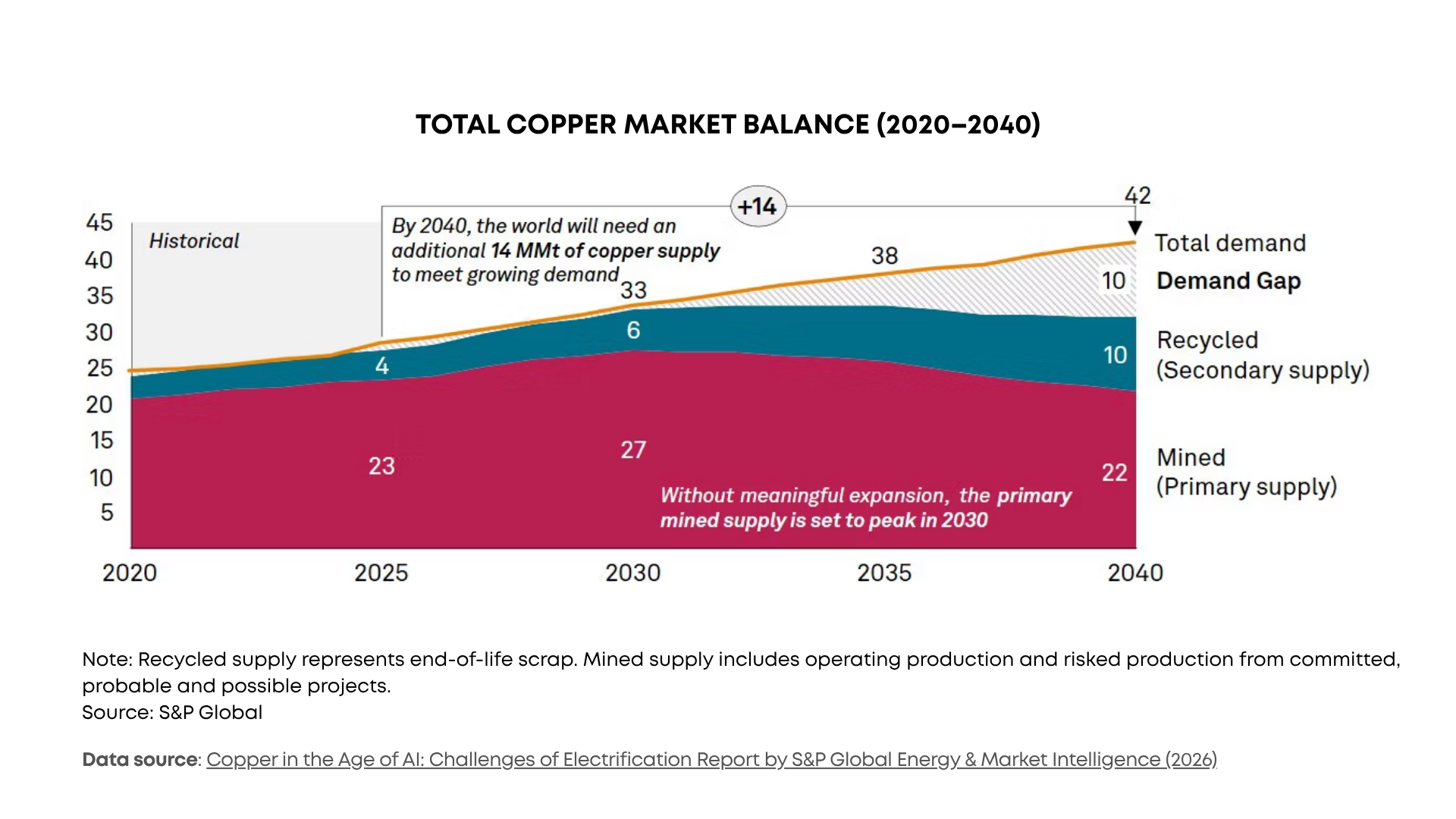

Let’s take copper as an example. It is mined in places like Chile, Peru, and the Democratic Republic of the Congo, often from increasingly low-grade ore that requires more energy and water to process. The ore is then treated using chemicals such as sulphuric acid, before being shipped to be refined, often in China. From there it is transported again to be turned into wiring, electronics, plumbing, and components for infrastructure, then sent to be assembled into products like electric vehicles, data centres, appliances, and renewable energy systems, packaged, and shipped to market. People (us) use these systems for decades, but eventually they need to be replaced, upgraded, or abandoned.

In the case of copper, it can be recycled many times without losing performance, but much of it is locked away in long-life infrastructure like buildings, cables, and pipes for 20 to 50 years or more. At the same time, a significant amount of copper is still lost through inefficiencies in recovery (think of all the electronics we throw away or keep in drawers and cupboards) or ends up mixed into complex waste streams and sent to landfill.

The difficulty is that our demand for the material outstrips our ability to supply it. It’s predicted that peak supply will be in 2030 leading to a growing demand for recycled copper. However, even with more efficient recycling, we’re looking at a large demand gap by 2040+. And this is just for the first generation of AI and renewable infrastructure roll out.

At each stage of the materials journey, there is wastage and losses including environmental, energy, material waste, or inefficiencies in production and distribution.

And as with energy, Jevons Paradox is at play. The more we have, the more we use. Efficiency has not reduced demand, it has accelerated it.

What looks like a simple material is in fact part of a complex, tightly coupled system. The more complex the system becomes, the more points of failure it contains. Just think about the number of components in a phone, a car, or even a household appliance. If one critical input is missing, the whole system slows or stops.

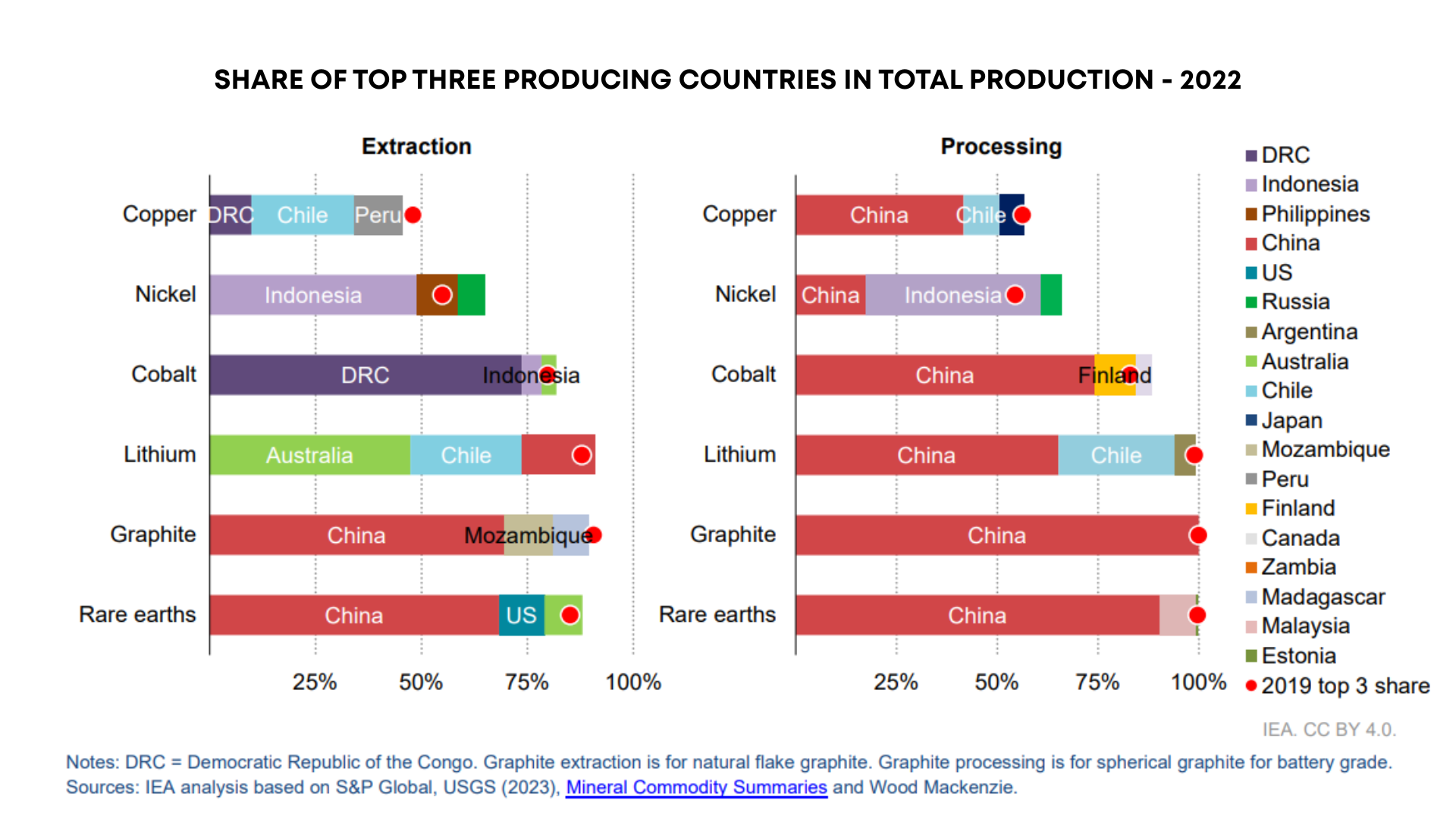

A key risk within this system is how concentrated extraction and production is in a small number of countries. Many critical minerals are dominated by just a handful of producers, meaning a single country can account for a large share of mining or processing, with refining often even more concentrated. This creates structural vulnerabilities, where geopolitical tensions, trade restrictions, or disruptions in one region can quickly ripple through global markets, affecting both price and availability.

Even before the current conflict, several critical materials such as copper, lithium, nickel, and rare earths were already facing structural pressure, with demand from electrification and digital infrastructure beginning to outstrip supply growth, compounded by declining ore quality and rising extraction costs.

This is the core challenge. We have built a system that is highly efficient, but not very resilient. When disruption occurs, whether through conflict, energy shocks, or supply constraints, the impacts cascade quickly across industries, economies, and everyday life.

Impact of the Iran Conflict

The recent conflict has highlighted the compounding nature of these limits and the fragility of the system. Bombing of key infrastructure as well as volatility in global markets is disrupting a wide range of critical industrial inputs. The conflict is disrupting both supply and infrastructure, limiting the movement of materials and reducing global availability, and some key facilities have been damaged. Some of the infrastructure that has been heavily damaged may take years to get back into operation. While the full extent of damage is not yet known, QatarEnergy has said that 17% of its Liquid Natural Gas (LNG) capacity has been wiped out for the next five years.

Materials directly affected include sulphur and sulphuric acid, helium, methanol, aluminium, and graphite, along with key fertiliser inputs and water treatment chemicals. as well as the petrochemical feedstocks used to produce plastics, which are particularly exposed. These all rely on fossil fuel production, petrochemical processing, and shipping routes through the Gulf.

As these flows are disrupted, the impacts cascade across food systems, healthcare, manufacturing, and the energy transition. What emerges is not a single supply shock, but a systemic disruption.

The immediate result is rising costs and increasing scarcity. Energy prices have increased. The availability of key materials has declined. These pressures are flowing through supply chains and pushing up prices globally.

Even if tensions ease in the near term, supply disruptions could take months to stabilise and several years to fully recover, with some impacts likely to persist long term as the system adjusts to tighter and more uncertain conditions. We are seeing a structural shift in the system.

Rising geopolitical tensions are reshaping global supply chains, forcing businesses to move away from purely cost-driven models toward ones focused on resilience and security. Companies are shifting from globalisation to more regional and diversified supply networks, holding more inventory, and investing in nearshoring to reduce risk. At the same time, digital tools are improving visibility and decision-making, while sustainability is becoming part of long-term strategy. Although these changes can increase costs and complexity, they are helping create more flexible and robust systems better suited to an uncertain global environment

Are We at Risk of Running Out of Materials?

The short answer is no, but with an important caveat. There are enough critical materials in the Earth’s crust in a broad geological sense, but not enough readily available supply to meet the rapid growth in demand from AI, electrification, and renewable infrastructure without bottlenecks, rising costs, and delays, even before factoring in geopolitical disruption and competition for resources.

The main constraint is not just “how much exists”, but whether materials can be mined, processed, financed, permitted, transported, and refined quickly enough. Extraction is closely tied to the availability and cost of fossil fuels, particularly oil, which underpins much of the equipment, transport, and processing involved. As oil becomes more complex and expensive to extract, this feeds directly into the cost and viability of producing other materials, shaping how much supply comes online and when. Ultimately, resources are only developed when they are economically viable, meaning higher costs can delay or limit new supply even when the materials themselves still exist.

Demand is fast outstripping supply. The IEA expects demand for key energy minerals to grow strongly by 2040, including lithium rising fivefold, graphite and nickel doubling, copper rising about 30%, and cobalt and rare earths rising 50 to 60% under current policy settings. AI adds pressure because data centres require large amounts of electricity, grid upgrades, backup systems, cooling, and copper-intensive infrastructure. The IEA says data centre electricity demand surged in 2025, with AI-focused data centres growing even faster.

So Should we be Mining More?

Mining and extraction come with significant environmental and social impacts. To access lower-grade and more remote resources, operations are expanding in scale and intensity, often leading to land disturbance, deforestation, habitat and biodiversity loss, destruction of food systems, and large volumes of waste. Many processes require substantial amounts of water and energy, while the use of chemicals in refining can create risks of soil and water contamination if not carefully managed. As higher-quality deposits decline, the environmental footprint per unit of material tends to increase, meaning more energy, more land, and more impact are required to produce the same output.

These impacts are often felt most directly by local communities. Mining can place pressure on water supplies, affect air and soil quality, and disrupt livelihoods, particularly in regions where agriculture or natural ecosystems are central to community wellbeing. While mining can bring jobs and economic activity, the benefits are not always evenly shared, and communities can be left managing long-term environmental and social consequences after projects end. This creates tension between the global demand for materials and the local realities of extraction.

This raises important ethical questions. Many of the materials enabling modern life and the transition to cleaner energy are sourced from places far removed from where they are ultimately used, and that disconnect can make it easy to overlook the true cost of extraction. Moves in Aotearoa to fast-track mining approvals bring the reality of these impacts into sharper focus, highlighting the tension between speed and scrutiny, while also reinforcing that robust, and sometimes slower, regulatory processes play an important role in ensuring better long-term decisions for communities and the environment.

As demand continues to grow, there is a responsibility to consider not just how much we extract, but how we extract it, who benefits, and who bears the impact. This points to the need for stronger standards, more transparent supply chains, and a greater focus on reducing demand, reusing materials, and designing systems that place less pressure on both people and the environment.

The Case for Urban Mining and the Circular Economy

With demand for critical materials looking to outstrip supply in the near future, we need to focus now on getting the circular economy up and running. The shift to a clean energy system will significantly increase demand for critical minerals such as copper, lithium, nickel, and cobalt.

Recycling is emerging as a critical pillar of supply security. It creates a secondary source of materials that reduces reliance on new extraction, helps diversify supply for import-dependent countries, and lowers exposure to geopolitical and supply chain risks . While recycling cannot fully replace mining, it can meaningfully reduce the scale of new mining required and act as a buffer against future disruptions.

Let’s take a relatable example. It’s estimated that there are billions of dollars worth of mobile phones in drawers around the world that are not being used. Every phone we have ever owned along with solar panel and battery being installed today contains critical materials. These should be thought of as a future resource. Even if the economic case for recycling is not there yet, it likely will be in the future. The question is where and how we store and manage these materials so they remain accessible for future use when urban mining becomes a necessity.

Beyond supply security, a circular economy approach delivers clear environmental and economic benefits. Recycled materials typically require far less energy, water, and emissions than primary production, and prevent valuable resources from being lost to landfill. Yet current recycling rates for many critical minerals remain low and are not keeping pace with rapidly rising demand. Scaling up recycling, alongside designing products for reuse, repair, and recovery, will be essential to reduce waste, improve system resilience, and build a more sustainable and secure materials system for the future.

What does this mean at the local level? We need to invest in setting up the infrastructure now that will enable the circular economy to scale up. Local resource management hubs such as Wastebusters as well as regional and national supply and transformation centres are vital pieces of infrastructure for the new economy.

Our Responsibility to the Future

We probably have enough materials in theory, but not enough accessible, affordable, and responsibly produced supply at the pace currently being demanded. This means society will need to prioritise , recycle far more, build more efficiently, and decide where scarce materials are best used. At the end of the day do we want more data centres, energy resilience, infrastructure repair, or new construction.

This also raises a deeper question about our responsibility to future generations. If we continue to extract and use materials at the current pace, it is increasingly likely that easily accessible, high-quality resources will become more constrained in 25, 50, 75, or 100+ years.

We need to start asking ourselves some key questions. Are we leaving our kids and grandkids access to sufficient materials to maintain, repair, and replace the systems we are building today, let alone meet new demand? While resources will still exist in the ground, they will be harder, more expensive, and more environmentally damaging to extract as time goes on. That means the choices we make now about how we use, reuse, and preserve materials will shape the options available to those who come after us.

WHAT THIS MEANS FOR AOTEAROA NEW ZEALAND

For New Zealand, the challenge is less about running out of materials entirely and more about exposure to a global system that is becoming more volatile, more expensive, and less predictable. We are the last bus stop on the planet with respect to supply chains and rely heavily on imports for many of the materials that underpin our economy. When disruption occurs, whether through conflict, energy shocks, or trade restrictions, the impacts arrive quickly in the form of higher costs, longer lead times, and reduced availability.

The materials most at risk are those that are both heavily imported and tied to energy, petrochemicals, and global processing hubs. This includes plastics and petrochemical products such as PVC used in pipes and construction, bitumen for roads and infrastructure, and fertiliser inputs that support agriculture. Metals like steel, aluminium, and copper are also exposed, particularly where processing is concentrated offshore. While New Zealand produces some steel and aluminium, much of this is exported as primary product, and we remain reliant on imports for a large share of finished and fabricated materials such as structural steel, reinforcing, and aluminium joinery. These materials are essential for building, maintaining infrastructure, electrification, and everyday goods, meaning even small disruptions can have wide-reaching effects.

What we are likely to see is not widespread shortages, but ongoing pressure across the system. Projects may take longer, costs will continue to rise, and substitutions may become more common. This creates a more constrained environment where planning, flexibility, and efficiency become increasingly important. For New Zealand, the risk is not just about access to materials today, but how we adapt to a future where supply is tighter, more complex, and less certain.

We are starting to see global suppliers respond to volatility in real time, with some now carving out large portions of contract value and refusing to fix prices due to uncertainty around energy, shipping, and raw materials. While international players are moving early, the domestic market is still catching up, with many contracts not yet reflecting this new level of risk. The result is increasing tension between fixed-price expectations and a reality where input costs can change quickly and significantly.

For contractors, this reinforces the need to move from a reactive to a proactive approach. Risk needs to be managed upfront, not passed on later. That means building escalation clauses into contracts at the outset, clearly defining how cost increases will be handled, and flowing those terms through the entire supply chain. As soon as a head contract is signed, commitments should be aligned with subcontractors and suppliers to avoid exposure. Managing relationships is no longer enough. Contracts need to reflect the new environment, with clear mechanisms for dealing with volatility.

For clients, this is a shift in expectations. Fixed-price certainty is becoming harder to achieve, particularly on longer or more complex projects. Instead, there is value in working collaboratively with contractors to agree fair and transparent escalation provisions from the start. This helps avoid disputes later and ensures projects remain viable. The focus should be on shared understanding of risk, realistic pricing, and building flexibility into agreements so that both parties can navigate a more uncertain and rapidly changing supply environment.

These challenges are significant, but they also create an opportunity to build more resilient, efficient, and locally adapted systems.

WHAT YOU CAN DO?

Individuals

Think compact and efficient. If you’re building or buying a new house, think about how much space do you need and will use? How many people are going to be living in the house? Smaller more compact spaces use less energy and resources. For new builds, it also helps you save on costs that you can put back into the quality of materials you use. Pack in as much insulation as you can to make use of passive solar gains.

Simplify designs to reduce material use. Size it up to standard material sizes so that there are fewer offcuts. Put the house on piles rather than using a slab to avoid increased concrete and excavation costs.

Reduce wastage. You pay for all materials that come onto site, those that go to building the house as well as everything going into the skip. Work with your architect, designer and builder to ensure money is not going in the bin.

Design and build the longterm - think of the house as a resource for future generations. How can you make it easier for them to reuse materials?

Prioritise energy efficiency - the higher the energy efficiency of your building, the less exposed you are to fluctuations in energy prices. Check out passive design and NZGBC Homestar standards. Be smart about using site orientation and design to keep the house warm in winter and cool in summer. Integrate “low tech” solutions like Puy Canadien for ventilation. Helps avoid unnecessary costly heating and cooling equipment. Overtime this will save you money.

Choose materials carefully - Source as many recycled or repurposed materials as possible. Look out for solid rimu doors, recycled timber cladding or flooring, get imaginative. Prioritise locally available natural materials where possible (timber, wool etc.), be aware of high risk materials in the supply chain and ensure you’ve ordered with increased time scales. Specify materials with multiple supply options. Minimise plastic-based materials where alternatives exist. This will reduce your exposure to toxic chemicals in the home. Think about paint, flooring, and other petrochemical products - they are hidden everywhere. At all costs, avoid materials with ingredients that are on the Red List.

Electrify the house - Don’t install any connections to fossil fuel heating or cooking facilities. This exposes you to volatile pricing and supply into the future. Electrify the house if you can. Install solar, and if you can, a battery. Keep in mind that at the end of their life, materials in these products may be in high demand. Keep maintained and in operation for as long as possible.

End of life stewardship - if you have products in your house that contain critical materials, don’t throw these in the bin. Find out where you can take these to be reused or recycled. If there is no avenue for this, advocate with your local council and at the national level to get something set up.

Businesses

Manage contracts proactively. Agree escalation clauses upfront. Clearly define how cost increases will be handled. Flow contractual commitments through to subcontractors and suppliers early. Avoid relying on fixed-price assumptions in a volatile environment.

Plan for disruption. Allow longer lead times for materials and delivery. Identify backup suppliers early. Build contingencies into budgets and timelines. Stage projects to manage risk

Design for longevity and simplicity. Think long term. Simplify designs and reduce unnecessary complexity. Build to last longer, be repaired, and be adapted over time. Avoid over-specification and design systems that use fewer materials and standard components.

Improve construction efficiency. Use prefabrication where possible to reduce waste and delays. Plan material use carefully to minimise offcuts. Reuse materials and components where practical. Reduce rework through better coordination

Support circular use of materials. Design for disassembly and reuse. Source recycled or reclaimed materials where possible. Keep materials in use rather than sending them to landfill. Work with suppliers who offer take-back or reuse options. Support initiatives like Wastebusters and advocate for version 2.0 C&D Materials Hub.

Collaborate. Get involved in groups like the Better Building Working Group to share information early between designers, builders, and suppliers. Take an integrated design approach to the build from the outset getting all those involved in the project on board to create efficiencies and avoid delays. Build long-term relationships with reliable suppliers.

YOU MADE IT - I HOPE YOUR CUPPA IS NOT COLD!

The challenges are real, but so is our ability to respond. Every choice, from how we design and build, to how we use and reuse materials, helps create a more resilient system. Small changes today, using less, wasting less, and thinking long term, add up over time. Together, we can turn uncertainty into an opportunity to build more resilient, efficient, and future-ready communities.